Business News of Saturday, 11 May 2024

Source: Togbe Afede XIV

Bank of Ghana profits unduly from high rates - Togbe Afede XIV

Togbe Afede XIV

Togbe Afede XIV

Background

On March 25, 2024, the Monetary Policy Committee (MPC) of the Bank of Ghana decided to maintain the policy rate at 29%, citing persisting upside risks to inflation. But the stark reality is that BOG is in a financial quagmire because it may find it difficult to meet its operating expenses when interest rates fall significantly, which, on the other hand, is necessary for sustainable high economic growth.

BOG’s “interest and similar income” amounted to GH₵5.09 billion in 2022, which was 92.7% of its total operating income of GH₵5.49 billion. Going by its 2022 financial statements, if BOG’s policy rate were to fall from 29% to 14.5% (still very high given its target of 8% inflation), BOG would lose close to half of its income and be unable to meet its operating expenses, of which staff costs alone amounted to GH₵1.62 billion, that is, GH₵735,361 per employee in 2022 or GH₵61,280 monthly per employee.

In announcing its March 25, 2024 decision, BOG explained that, “Despite a sharp deceleration in 2023, the pace of disinflation has moderated in the first two months of the year. While inflation experienced a slight uptick in January 2024 followed by a marginal decrease in February, the latest forecasts indicate a potentially elevated trajectory”. The bank added that, “Factors contributing to this outlook include possible adjustments in transport fares, utility tariffs, higher fuel prices and the pass-through effects of exchange rate depreciation”.

The truth is, all these variables are related. Whilst the policy rate is an important tool of monetary policy, its misuse, as in our case, can have damaging effects. As long as interest rates are kept unnecessarily high, our currency, the cedi, will continue to suffer adverse consequences, with pass-through effects on other prices, including transport fares, utility tariffs and fuel prices. Persistent cedi depreciation has been a key factor in our energy (including power) sector problems. We have always felt the need to adjust prices, not because consumers were not paying enough, but because the cedi has been depreciating.

The bank further stated, “Headline inflation has demonstrated relative stability since December 2023, with a decline to 23.2 percent in February from 23.5 percent in January 2024. This decrease was driven by reductions in both food and non-food inflation, signalling broad-based easing in underlying inflationary pressures”. Well, let us wait and see what will be recorded for March 2024, given that the consumer price index (CPI) fell by 1.2% in March 2023.

BOG concluded that their monetary policy rate decision underscores their commitment to balancing economic stability amid persistent “inflationary risks” and supporting sustainable growth of the economy. But economic stability and sustainable high growth will remain elusive as long as interest rates stay astronomically high.

BOG needs high-interest income to fund excessive spending

The reality, as I stated in my most recent article, is that BOG, given its excessive operating and other expenditures, may not be able to hold its own in a low-interest rate environment. So, the Bank has the incentive to keep its policy rate high to protect its main revenue source – interest income. Its “interest and similar income” amounted to GH₵5.09 billion (net GH₵1.8 billion) in the difficult post-COVID 2022, up 47% from GH₵3,46 billion in 2021, and was 92.7% of its operating income of GH₵5.49 billion.

Details of BOG’s 2022 annual report say a lot about our mentality. Budgeted expenditure of US$ 250 million for their new head office, equivalent to 0.35% of our GDP, sounds insane in a small and struggling country. The same can be said of the reported expenses:

GH₵97.4 million for travel; GH₵131 million for motor vehicle maintenance/running; GH₵32 million for communication; GH₵67 million “computer related”; GH₵207.7 million for premises and equipment; GH₵336.9 million for currency issue (currency in circulation amounted to GH₵40.73 billion); GH₵287.83 million for other administrative expenses, etc.

The Bank’s personnel costs amounted to GH₵1.62 billion. With a total of 2,203 employees, this equals an average remuneration of a colossal GH₵735,361 per employee in 2022 or GH₵61,280 monthly per employee, including several allowances. These employees also had staff loans amounting to GH₵1.247 billion, an average of GH₵566,046 per head.

BOG is also reported to be remodelling its regional offices, while investing GH₵142 million in a 50-bed guest house in Tamale.

BOG and its staff are living in a completely different reality. Apart from its excessive operating expenses, proper cost-benefit analysis would not justify its colossal investments in a new head office building and in non-core activities like a hospital and guest houses.

With a GH₵55 billion negative net worth, BOG is indeed in a quagmire and would be reluctant to see interest rates fall quickly at this critical time when it needs to make more money to survive. And its new tiered Cash Reserve Ratio (CRR) system should bring it more free cash for its exploitative and predatory lending activities. This is in addition to its power to print money.

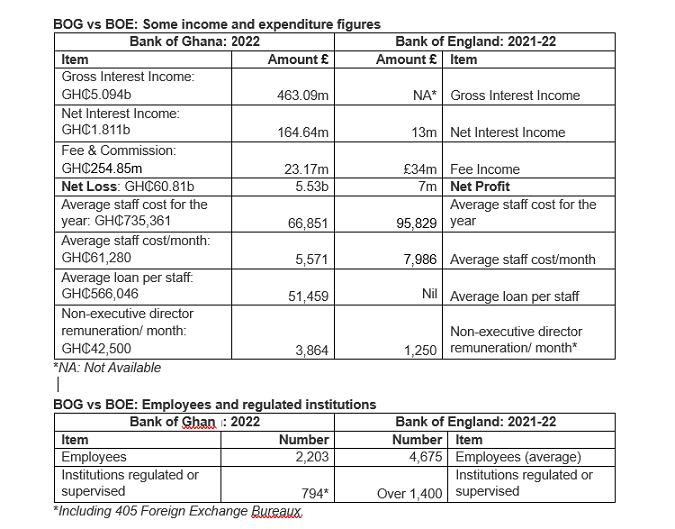

BOG vs Bank of England (BOE) – A case of the poor living like the King!

It is difficult to believe how some BOG’s operating incomes and expenses compare with those of Bank of England (BOE). For example, BOG spent GH₵1.62 billion (£147.27 million at 2022 average cedi-pound exchange rate) on its 2,203 employees, that is, £66,851 per employee, about 38x Ghana’s GDP per capita. BOE on the other hand, with an average labour force of 4,675 per their 2021-22 financial report, spent £448 million, that is, £95,829 per employee, about 2.6x UK’s GDP per capita.

Unlike BOE staff who do not receive loans from their employer, BOG staff owe the bank GH₵566,046 (£51,459) on average or per employee as at the end of 2022.

BOE’s reports disclose the remuneration of individual executives, but BOG’s financial statements do not. So, a comparison of individual executive remuneration is not possible.

But BOG’s non-executive directors earned 3x what their BOE counterparts earned in 2022. BOG’s ten (10) non-executive directors earned GH₵5.1 million in 2022, averaging GH₵510,000 (£46,364) per director for the year, or GH₵42,500 (£3,864) per month.

BOE’s statement on the remuneration of non-executive directors shows that its rates, which were effective from June 1, 2009, were set at £15,000 per annum (£1,250 per month) for non-executive directors. Committee Chairs receive a little more. Non-executive directors do not receive any additional fees for serving on Committees.

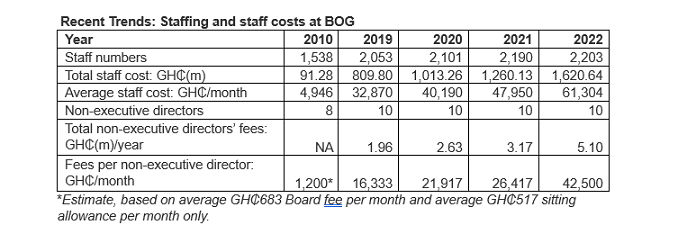

It is difficult to imagine how the technically bankrupt institution is funding its exorbitant expenditures. BOG’s extravagance is typical of poorly supervised cash-rich stateowned enterprises, many of which increase remuneration and expenditures at will, as shown by the trend in staff numbers and costs at BOG captured below:

BOG’s staff strength went up 43% between 2010 and 2022. Average staff cost went up 1,100% and fees per non-executive director went up 3,400% over the same period.

So, budget considerations appear to be a factor in BOG continuously keeping interest rates high, even when they are targeting or expecting single-digit inflation. The last reduction in the policy rate was a laughable 1%, from 30% to 29%.

Mopping up excess liquidity?

BOG’s “mopping up excess liquidity” explanation for its high monetary policy rate is not convincing. “Excess liquidity” presumes a certain optimal liquidity that has still not been defined. Secondly, supply-side rather than demand-side factors are at the root of our inability to achieve sustained low inflation. Thirdly, it is difficult to persuade people to save when they are struggling to make ends meet.

It is surprising, therefore, that the IMF insists on these high interest rates that have not worked for us, the reason why we are engaging them for the seventeenth (17th) time!

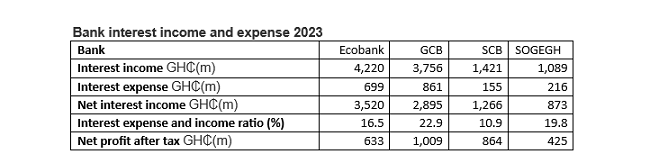

In any case, it is obvious from the table below that the banks do not share their high-interest income with depositors to encourage them to save:

It is noteworthy that a lot of these banks’ average cost of funds are less than 8%. But, taking advantage of BOG’s high policy rate, they lend to their customers at 36% or more. BOG often boasts about growing banking sector assets, but these are mostly growth in cedi terms, fueled by high interest rates and inflation.

Meanwhile, the Government is still borrowing at very high rates: 91-day Treasury Bills at 25.75%; 182-day at 28.25%; and 365-day at 28.85%.

Harmful effects of BOG’s monetary policy

Cedi depreciation:

The cedi has experienced an average depreciation of 6.2% year-to-date “against major trading currencies such as the US Dollar, British Pound, and Euro”, as per the latest data from BOG. It would be disingenuous to attempt to draw any comfort from a comparison with what we experienced during the turbulent first quarter of last year, let alone suggest consequently that we are doing well.

The bad news is that, the recorded cedi depreciation roughly tracked the yield on Government of Ghana treasury bills, confirming that parity laws have been at work, just as we saw in 2023, when the cedi depreciated 27.8% against the US dollar. So, at current ridiculously high interest rates, our currency will continue to depreciate, to restore parity. It would be naïve to expect otherwise.

Inflation:

Cedi depreciation has had and will continue to have “pass-through effects on other prices, including transport fares, utility tariffs and fuel prices inflation”. The generally lower yearon-year inflation figures of the past few months are not worth celebrating because they were influenced largely by what happened in the past rather than by current price changes. Thus, drop in year-on-year inflation in November 2023 to 26.4%, from 35.2% in October 2023, for example, was influenced largely by the 8.6% rise in the CPI in November 2022.

Year-on-year inflation statistics are useful to the extent that they have information value with regards to the future. Unfortunately, this is not usually the case in a volatile economic environment, and their evaluation needs to be tempered with current trends in the CPI.

The real sectors, growth and employment

It was revealed at a recent German Development Agency’s (GIZ’s) national stakeholder forum on AfCFTA, digital trade, and E-commerce organised in Accra that “Ghana is gradually becoming a net receiver of goods and services exported under the Africa Continental Free Trade Area (AfCFTA), nearly two years after piloting the guided trade initiative (GTI)”. This was attributed to the inability of Ghanaian businesses to take advantage of the continental free trade agreement to export to other countries in the jurisdiction.

This is not surprising given the high cost of doing business in Ghana, with interest rates being a major factor. This has serious implications for growth and job creation.

Need for restructuring at BOG

BOG requires drastic restructuring to make its operations more efficient, and to align its objectives to those of the state and ensure a sincere pursuit of stability. Maintaining a high-interest rate environment that ensures that our banks, including BOG, make abnormal profits at the expense of the real sectors is not good central banking practice.

A central bank’s raison d’etre is not profits, but stability, where BOG has failed woefully, even though corruption and poor fiscal policy and general macroeconomic mismanagement are contributory factors.

Restructuring is necessary at BOG, if it should be capable of surviving in a normal interest rate environment. Attention should be paid to its governance system, staff numbers and costs, procurement practices, growing obligations to former staff, and mandate.

Regarding its mandate, there is a strong case for BOG relinquishing its government treasury management function (to focus on regulation) because of conflict with its profit motivation.

Many other state-owned enterprises, including the once profitable Ghana International Bank, London, which has recorded massive losses recently, require serious attention. Many of them have recorded the kind of massive growth in staff numbers and costs that we have seen at BOG.

Entertainment